Auto Rollover FAQs

Got QUESTIONS? We’re here to help.

Below are some frequently asked questions about auto rollover IRAs. If you don’t find what you’re looking for, please contact us at 1.800.486.6888 or via our contact form.

Investor Services Hours:

Monday – Thursday: 7am-5pm CST

Friday: 7am-4pm CST

What is required of Plan Sponsors who choose the Safe Harbor Automatic Rollover provision?

In general, if a Plan Sponsor chooses to adopt the Safe Harbor Automatic Rollover provision, it must:

a) Amend the plan to provide for the automatic IRA rollover provision.

b) Distribute a SMM (Summary of Material Modifications) to plan participants.

c) Select an IRA provider to handle automatic rollovers.

d) Have a signed agreement with the IRA provider in place.

e) Establish processes and procedures to accommodate automatic rollovers by the time the first automatic rollover is to be processed.

How does GoldStar attempt to locate lost or missing participants once the Automatic Rollover IRAs have been established?

Once the IRA has been established for the lost or missing participant, a Welcome Letter is mailed to the last known mailing address that explains who we are, why their retirement funds have been rolled over to GoldStar and how the funds can be claimed. Ongoing search tools are utilized to locate the missing participants if we don’t receive a response on the first attempt. All search results are documented and maintained for audit purposes.

What happens if the rollover remains unclaimed?

Each year, GoldStar submits its database to a search firm, in an attempt to reconnect account holders with their IRA accounts. Attempts are made annually, until such time as the account becomes subject to state abandoned property laws.

Is there a cost to the Plan Sponsor?

No, there is no cost to the plan sponsor to move the accounts.

Who will serve as the Custodian for the Automatic Rollover IRAs?

GoldStar Trust Company will serve as Custodian for the Automatic Rollover IRAs. GoldStar Trust is a trust only branch of Happy State Bank and has provided custodial trust services for Self Directed IRAs for over 25 years.

Is there an administrative fee assessed to the individual Automatic Rollover IRAs?

Yes, there is a nominal fee that is assessed annually on each account. This fee covers the administrative cost of searching for the participant and maintaining records for the DOL.

Is there a minimum account balance that can be rolled over to the GoldStar Trust Company Automatic Rollover IRA?

GoldStar accepts all account balances for Automatic Rollover IRAs; there is no minimum.

Is there minimum information we must provide about the participant to establish an account?

Yes, the participant’s name, date of birth, and social security number are required to establish an account and we request the participant’s last known address, if available.

As an employer, how should I attempt to locate lost or missing participants before establishing an Automatic Rollover IRA for the participants?

The DOL provides the guidance for fiduciaries that must be followed to locate lost or missing participants. When selecting GoldStar Trust Company as Custodian for Automatic Rollover IRAs, we will assist the employer with:

- Notification by mail and/or electronic mail to the last known address

- Two different commercial locator services

How does a plan sponsor select an IRA provider?

Plan sponsors may choose any IRA provider that meets the DOL’s requirements.

What are the plan sponsor’s responsibilities once the participant’s account is rolled into a safe harbor IRA?

Once the IRA provider establishes the participant’s account and the account is funded, under the DOL’s safe harbor rules, the plan sponsor will no longer be responsible for the account.

Why should Plan Sponsors want to force distribution on terminated participants?

There are a number of reasons for a Plan Sponsor to rid the Plan of small account balances of former employees, including:

- Prevent the need to file as a large plan, avoiding expense of an audit

- Accelerate access to forfeiture dollars by forcing distribution, there is no need to wait for the occurrence of 5 breaks in service before forfeiting

- Eliminate disclosure / communication requirements with former employees

- Minimize lost participants in the case of plan termination

- Reduce administrative costs, for plans paying administrative expenses based on the number of Participants in the Plan.

- Minimize potential exposure as a fiduciary under the DOL regulations

What kinds of distributions are eligible to be automatically rolled over to an IRA?

Distributions of a participant’s vested account balance of less than $5,000 that are made without the participant’s consent (often called “involuntary cash-out distributions”), must be rolled over to an IRA.

Contributions in the Qualified Plan, categorized as Roth, must be rolled over to a Roth IRA.

What about amounts greater than $5,000?

For terminating Defined Contribution Plans, the DOL has advised that plan fiduciaries can transfer individual retirement plan assets to individual retirement accounts (IRAs) if, after taking all prescribed steps to locate the owner, the owner cannot be found.

These prescribed steps include using certified mail, checking other employer plans and employer records, checking with a designated plan beneficiary for the individual’s whereabouts. In addition, fiduciaries should make reasonable use of free electronic search tools.

For more information, check out the Department of Labor Field Assistance Bulletin, FAB 2014-01.

What is the fiduciary liability with regard to the Automatic Rollover IRAs?

As long as the Department of Labor’s (DOL) Fiduciary Safe Harbor is satisfied, the fiduciary’s obligations with respect to the participant’s benefit end immediately upon the transfer of the benefit to the IRA.

Does the Qualified Retirement plan document need to be amended before the distributions are rolled over to the Automatic Rollover IRA?

It depends on the language in the plan document.

Are there issues associated with the USA PATRIOT Act of 2001 in establishing an IRA since the participant won’t be available to verify his or her identity?

No. The customer identification and verification requirements of the USA PATRIOT Act of 2001 apply only when the former participant or beneficiary first contacts the custodian to assert ownership or exercise control over the account.

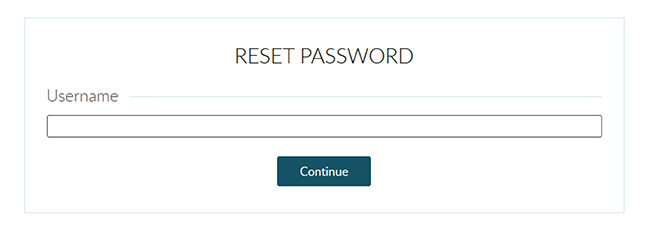

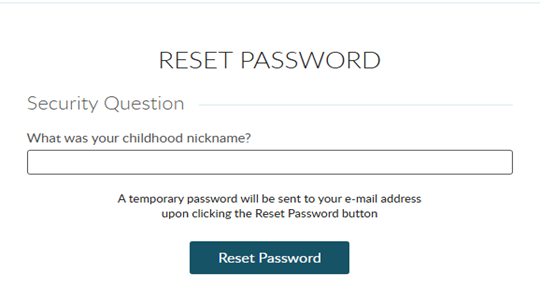

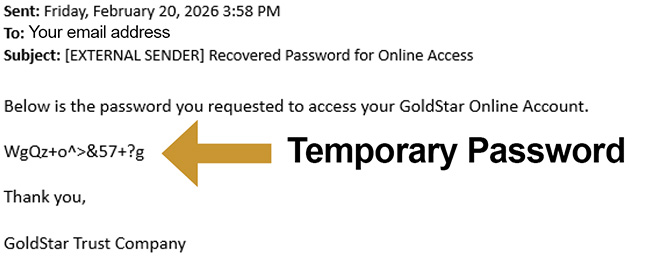

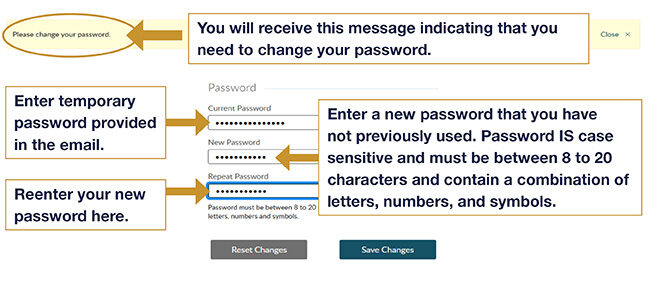

What happens when missing participants are located?

A simple online process allows them to claim their retirement funds held in a self-directed IRA established for them at GoldStar Trust.

What happens to the transferred funds?

Automatic Rollover funds are placed in a FDIC-insured, demand deposit account at GoldStar for each missing participant where balances earn a modest rate of return. GoldStar charges an annual fee (the lowest in the industry) deducted automatically from IRA balances. When we find them, participants can request a distribution or explore multiple investment options once they take control of their new IRAs.